Quick answer: HSA wins for long-term wealth; FSA wins for predictable current-year expenses.

If you qualify for an HSA and can manage the higher deductible of a qualifying health plan, the HSA is usually the stronger account because the balance rolls over forever, stays with you after job changes, and can be invested. An FSA is still useful when you have predictable medical, dental, vision, or childcare expenses and want immediate pre-tax savings through your employer.

The right choice is not only about the contribution limit. It depends on your health plan, expected healthcare use, employer contributions, tax bracket, cash flow, and risk tolerance. A high-income household with low medical utilization may treat the HSA as a tax-advantaged investment account. A family with predictable orthodontia, prescriptions, or planned procedures may still benefit from an FSA, especially when an HSA-qualified health plan is not available.

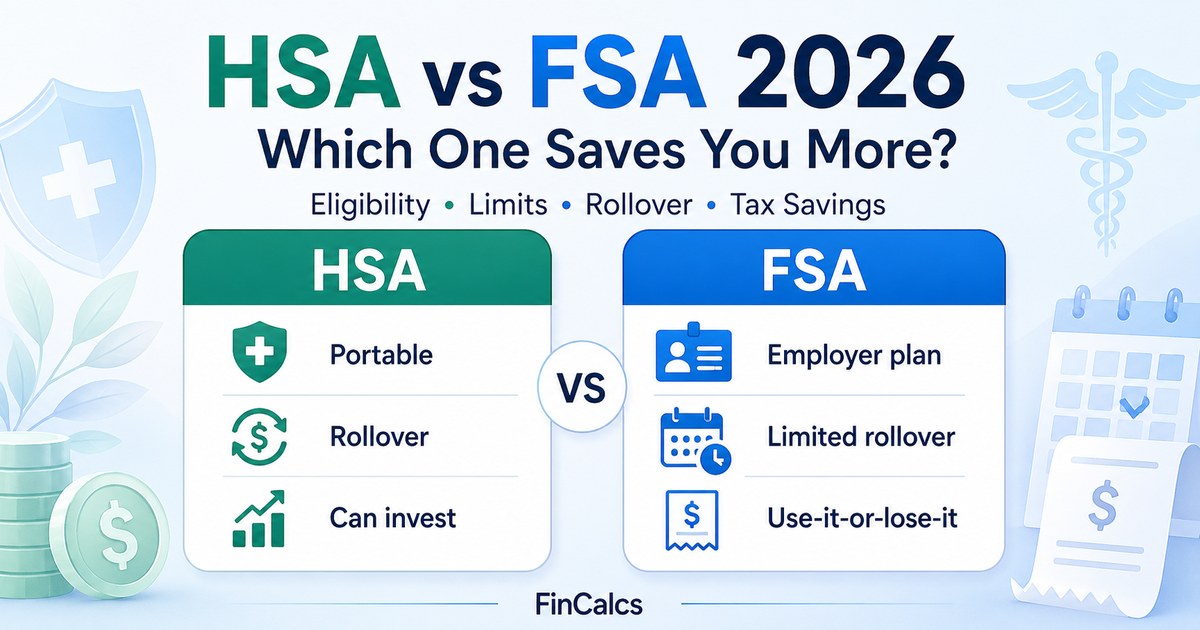

HSA vs FSA 2026: the core difference

An HSA, or health savings account, is a portable tax-advantaged account available to people enrolled in a qualifying high-deductible health plan. The money belongs to you, rolls over indefinitely, and can be invested for future medical expenses. That ownership feature is the main reason HSAs are often treated as both a healthcare account and a long-term planning tool.

An FSA, or flexible spending account, is an employer-sponsored pre-tax spending account. It can reduce your taxable income for eligible medical expenses, but unused money may be forfeited unless your employer allows a limited carryover or grace period. FSAs are powerful when your expenses are predictable, but they require more careful forecasting because overfunding can create a real loss.

In practical terms, the HSA is better for people who can tolerate uncertainty and want long-term compounding. The FSA is better for people who already know they will spend the money during the plan year. The HSA rewards patience; the FSA rewards accurate budgeting. Neither account is universally correct without looking at the health plan behind it.

Bottom line

Choose the HSA if you are eligible and want long-term flexibility. Choose the FSA if you do not qualify for an HSA or you have predictable healthcare expenses you expect to use during the same plan year. Consider an HSA + limited-purpose FSA combination if you are HSA-eligible and also have predictable dental or vision expenses.

2026 HSA and FSA contribution limits

For 2026, the HSA contribution limit is $4,400 for self-only coverage and $8,750 for family coverage. People age 55 or older can add a $1,000 catch-up contribution. For healthcare FSAs, the 2026 employee contribution limit is $3,400. Employers that allow a healthcare FSA carryover may allow up to $680 to carry into the next plan year.

These numbers matter, but the decision is not simply “which account lets me contribute more.” The HSA contribution limit is higher for family coverage and the money can accumulate across years. The FSA limit is lower, but an FSA can still be valuable because the tax savings occur immediately through payroll deductions. The main tradeoff is permanence: HSA money remains yours, while FSA money is tied to the employer plan and may expire.

| Account | 2026 contribution limit | Catch-up | Rollover | Best use case |

|---|---|---|---|---|

| HSA: self-only | $4,400 | $1,000 if age 55+ | Unlimited | Long-term medical savings and investing |

| HSA: family | $8,750 | $1,000 if age 55+ | Unlimited | Family healthcare savings and retirement medical planning |

| Healthcare FSA | $3,400 | None | Limited: up to $680 carryover or grace period if employer allows | Predictable medical, dental, and vision expenses this year |

| Dependent Care FSA | Plan- and law-dependent; commonly used for childcare expenses | None | Usually use-it-or-lose-it | Daycare, preschool, before-school or after-school care, and eligible dependent care |

Source note: HSA limits and HDHP thresholds are based on IRS 2026 inflation-adjusted HSA guidance. Health FSA limits depend on employer plan design, so employees should confirm their plan rules during open enrollment.

Eligibility: who can use an HSA or FSA?

HSA eligibility

To contribute to an HSA, you generally need to be enrolled in a qualifying high-deductible health plan and avoid disqualifying coverage. For 2026, an HDHP generally must have a deductible of at least $1,700 for self-only coverage or $3,400 for family coverage. The plan must also satisfy the applicable out-of-pocket maximum rules. In ordinary household planning, this means the HSA decision begins with the health plan, not the account.

A person may like the HSA tax treatment but still decide against an HDHP if the expected total healthcare cost is too high. For example, a family with frequent specialist visits, expensive medications, or predictable procedures should compare premiums, deductibles, co-insurance, employer HSA contributions, and maximum out-of-pocket exposure. The HSA can be valuable, but it should not blind you to the risk of underestimating medical use.

FSA eligibility

A healthcare FSA is offered through an employer. You do not need a high-deductible health plan to use one. However, if you are covered by a general-purpose healthcare FSA, that coverage can interfere with HSA eligibility. This is why employees should review the exact FSA type during open enrollment. A regular healthcare FSA is different from a limited-purpose FSA, and that distinction matters.

Important compatibility rule

You generally cannot pair an HSA with a regular healthcare FSA. But you may be able to pair an HSA with a limited-purpose FSA that covers dental and vision expenses only. You may also be able to use a dependent care FSA because dependent care expenses are separate from medical HSA eligibility rules.

Rollover rules: the HSA’s biggest advantage

The most important difference is not the annual contribution limit. It is what happens to unused money. HSA funds roll over indefinitely. FSA funds are usually subject to use-it-or-lose-it rules, with only limited flexibility if the employer offers a carryover or grace period. This one rule changes the entire financial character of the account.

With an HSA, an unused dollar remains an asset. It can be saved for next year, used for a future medical bill, invested for long-term growth, or preserved for retirement healthcare costs. With an FSA, an unused dollar may become a deadline problem. You may need to spend it before the plan year ends, or you may lose it if your employer does not allow a carryover or grace period.

This is why HSA contribution decisions can be more aggressive than FSA contribution decisions. If you overestimate your HSA need, the unused balance simply remains yours. If you overestimate your FSA need, you may be forced to spend on less important items or risk forfeiture. The FSA is still useful, but it works best when the planned expense is known in advance.

| Feature | HSA | Healthcare FSA |

|---|---|---|

| Unused money after year-end | Stays in your account indefinitely | May be forfeited unless carryover or grace period applies |

| Job change | You keep the account | Generally tied to the employer plan |

| Investment option | Often available after a cash threshold | Not available |

| Retirement planning value | High | Low |

Tax savings: both accounts help, but HSAs go further

Both HSAs and FSAs can reduce taxable income when contributions are made through payroll. The HSA has a broader tax advantage because contributions can be tax-deductible, growth can be tax-free, and withdrawals for qualified medical expenses can also be tax-free. That combination is why HSAs are often described as one of the most tax-efficient accounts available to households with eligible health plans.

HSA tax advantage

HSAs are often described as having a triple tax advantage: contributions can reduce taxes, investment growth can be tax-free, and qualified medical withdrawals can be tax-free. This makes the HSA unusually powerful for people who can afford to contribute more than they spend in the same year. The unused balance can become a long-term healthcare reserve, especially for retirement, when medical costs often become more important.

The strongest HSA strategy is to contribute through payroll when available, keep enough cash in the HSA for near-term medical costs, invest the excess if the provider allows it, and avoid using the account for small current expenses unless cash flow requires it. This approach turns the HSA from a spending account into a compounding account.

FSA tax advantage

FSAs provide immediate tax savings on money you expect to spend during the year. The tradeoff is that unused funds can be lost, so the optimal FSA strategy is usually conservative: contribute only what you are highly confident you will use. Good FSA candidates include predictable prescriptions, planned dental work, orthodontia, eye exams, glasses, contacts, scheduled procedures, and recurring copays.

The FSA advantage is behavioral as well as mathematical. Because the money is set aside before expenses occur, households can budget for medical costs more intentionally. The risk is that the account can encourage unnecessary year-end spending if too much money remains. For that reason, the safest FSA election is usually based on confirmed or highly likely expenses, not a vague estimate.

The HSA investment advantage

The HSA’s most powerful feature is not just tax savings. It is the ability to let unused money compound over time. A person who contributes consistently and invests the HSA balance can turn the account into a long-term healthcare reserve for retirement. This is fundamentally different from an FSA, which cannot be invested and is generally tied to current-year spending.

Consider two households that each set aside money for healthcare. The first household uses an FSA and spends the balance each year. That household receives a useful tax benefit, but the account does not build long-term wealth. The second household uses an HSA, pays smaller medical expenses from regular cash flow when possible, and invests the HSA balance. Over many years, the second household may accumulate a meaningful reserve for future medical costs.

That does not mean every family should automatically choose the highest-deductible plan. The right decision depends on premiums, expected medical expenses, employer contributions, cash flow, and risk tolerance. But if the total health plan cost is reasonable, the HSA often has a superior long-term profile. The account is especially attractive for people who are healthy, have emergency savings, receive employer HSA contributions, or already contribute enough to other retirement accounts.

When an FSA can make more sense

The HSA is stronger for long-term wealth, but the FSA is not useless. It can be the better practical choice in several common cases. The key is to stop treating the decision as a contest between account names and instead evaluate your actual health plan, cash flow, and expense pattern.

1. You are not HSA-eligible

If your health plan is not HSA-qualified, an FSA may be the only available pre-tax healthcare spending account. In that case, an FSA can still reduce taxes on medical expenses you expect to pay. A household with a strong low-deductible plan, predictable doctor visits, and recurring prescriptions may be better off using an FSA than switching to a high-deductible plan just to access an HSA.

2. You have predictable expenses this year

Scheduled dental work, orthodontia, prescription costs, planned procedures, eye exams, glasses, or contacts can make an FSA valuable because the money is likely to be used before year-end. The more predictable the expense, the lower the risk of forfeiting unused funds. A planned dental crown, a known prescription schedule, or a child’s orthodontia treatment can make an FSA election straightforward.

3. Your employer offers a strong low-deductible plan

Some employers subsidize low-deductible health plans heavily. In those cases, the best overall benefit package may be the low-deductible plan plus FSA, rather than switching to an HDHP just to access an HSA. This is especially true when the HDHP premium savings are small or when the out-of-pocket risk is high relative to the household’s emergency savings.

4. You need short-term certainty more than long-term compounding

The HSA is excellent when you can wait. The FSA is useful when you cannot. A household facing near-term medical bills may value immediate payroll tax savings more than long-term investment flexibility. Personal finance decisions are not only about theoretical maximum wealth; they are also about liquidity, stress reduction, and avoiding avoidable cash-flow shocks.

HSA + limited-purpose FSA: the best of both worlds

Many people miss this strategy: you may be able to use an HSA and a limited-purpose FSA together. A limited-purpose FSA is generally restricted to dental and vision expenses, so it does not create the same HSA conflict as a general-purpose healthcare FSA. This can be a strong combination for families with predictable dental or vision costs.

The logic is simple. You preserve the HSA for long-term growth while using the limited-purpose FSA for expenses you already know are coming. Examples include dental cleanings, fillings, orthodontia, eye exams, glasses, and contact lenses. Instead of withdrawing HSA dollars for those routine costs, you use limited-purpose FSA dollars and allow the HSA to remain invested.

This strategy works best when you can forecast dental and vision expenses with reasonable confidence. It does not eliminate the need to avoid overfunding the FSA. But it does provide a way to combine the HSA’s long-term compounding advantage with the FSA’s immediate payroll-tax savings on predictable spending.

Dependent Care FSA: separate from the healthcare decision

A dependent care FSA is different from a healthcare FSA. It is generally used for eligible dependent care expenses such as daycare, preschool, before-school care, after-school care, and certain day camps so that a parent or guardian can work or look for work. Because it covers dependent care rather than medical expenses, it is separate from the HSA versus healthcare FSA compatibility issue.

This means some households may use an HSA for medical expenses, a limited-purpose FSA for dental and vision, and a dependent care FSA for childcare. That combination can be highly tax-efficient, but it also requires careful planning. Each account has different rules, eligible expenses, deadlines, and documentation requirements.

Families should be especially cautious about dependent care FSA elections because childcare needs can change during the year. A child may start school, switch programs, or have a change in summer care. The best election is based on realistic expected expenses rather than simply choosing the maximum.

Decision framework: choose HSA, FSA, or both?

The best way to decide is to model the health plan first and the account second. Compare the monthly premium, employer HSA contribution, deductible, co-insurance, expected healthcare use, prescription costs, and worst-case out-of-pocket exposure. Then layer in the tax savings from the HSA or FSA.

If the HDHP has meaningfully lower premiums and your employer contributes to the HSA, the HSA may win even before considering investment growth. If the HDHP barely reduces premiums and exposes you to a much higher deductible, the FSA with a lower-deductible plan may be more practical. The best decision is the one that balances tax efficiency with risk control.

| Your situation | Likely better choice | Why |

|---|---|---|

| You qualify for an HSA and can handle the deductible | HSA | Higher limits, unlimited rollover, portability, and investment potential |

| You have predictable medical expenses this year | FSA or HSA + limited-purpose FSA | Immediate tax savings with lower risk of unused funds |

| You are not enrolled in an HSA-qualified plan | FSA | FSA may be the available pre-tax healthcare account |

| You want to invest for future healthcare costs | HSA | FSA money cannot be invested and may expire |

| You have dental and vision expenses while HSA-eligible | HSA + limited-purpose FSA | Preserves HSA growth while using pre-tax dollars for dental and vision |

FinCalcs recommendation

Start with health plan economics, not the account name. Compare premiums, deductibles, employer HSA contributions, expected medical costs, and tax savings. If the HDHP is financially reasonable, the HSA usually provides the best long-term value. If your expenses are predictable and your employer plan is not HSA-compatible, use the FSA carefully and avoid over-contributing.

Open enrollment checklist

Open enrollment is the best time to make the HSA versus FSA decision because many of the inputs are available at once: plan premiums, deductibles, employer contributions, FSA limits, expected family needs, and next-year medical appointments. Use this checklist before selecting your benefits.

- Estimate next-year healthcare use. Include prescriptions, primary care, specialists, therapy, dental work, vision needs, planned procedures, and known family changes.

- Compare total plan cost. Add annual premiums and expected out-of-pocket costs, then subtract any employer HSA contribution.

- Evaluate emergency savings. An HDHP may be attractive, but it can be stressful if you cannot cover the deductible when care is needed.

- Separate medical from dental and vision. This helps identify whether a limited-purpose FSA can complement an HSA.

- Be conservative with FSA elections. Overfunding an FSA can create forced spending or forfeiture. Start with expenses you are confident will occur.

- Use calculators before finalizing. Model your tax bracket, employer contribution, expected expenses, and long-term HSA growth before choosing.

Common mistakes to avoid

Mistake 1: Choosing the HSA only because the tax treatment is better

The HSA tax structure is powerful, but the health plan still matters. A household with high expected medical use may find that a low-deductible plan plus FSA creates a better total cost outcome than an HDHP plus HSA. Always compare total cost, not only tax benefits.

Mistake 2: Overfunding the FSA

The FSA should be funded based on predictable spending. It is better to underfund slightly than to overfund significantly and risk forfeiture. A good rule is to start with recurring prescriptions, confirmed appointments, expected dental and vision expenses, and planned procedures.

Mistake 3: Forgetting the employer contribution

Some employers contribute to HSAs. That contribution can materially change the comparison. A plan that looks risky before the employer contribution may become attractive after it. Conversely, an HDHP without an employer contribution may be less compelling if the premium savings are small.

Mistake 4: Spending HSA dollars too quickly

Using an HSA for current medical expenses is allowed, but it may reduce the long-term advantage. If you can pay smaller expenses from cash flow, preserving and investing the HSA may create more value over time. This approach is not required, but it is often the strategy that turns an HSA into a true wealth-building account.